CBDC Development and Private Crypto Competition: Who’s Really Winning in 2026?

By early 2026, the battle for the future of money isn’t happening on crypto forums anymore-it’s happening in central bank boardrooms. While Bitcoin and Ethereum still grab headlines, governments are quietly building something far more powerful: Central Bank Digital Currencies (CBDCs). And they’re not just keeping pace with private crypto-they’re outmaneuvering it in ways most people don’t realize.

CBDCs Are No Longer Experimental

In 2023, only 114 countries were looking into CBDCs. By January 2026, that number jumped to 134-covering 98% of global GDP. This isn’t a trend. It’s a global reset. From the Bahamas to Nigeria, Jamaica to Zimbabwe, 11 countries have already launched their own digital currencies. Another 69 are in active pilot stages. Even major economies like Japan and India are running multi-year pilots with millions of users testing offline payments, real-time settlements, and programmable money features. The Reserve Bank of India now offers both retail and wholesale CBDCs. Japan’s Bank of Japan has spent over two years refining user interfaces, ensuring accessibility for elderly citizens and rural populations. These aren’t prototypes. They’re working systems being stress-tested under real conditions.Why CBDCs Beat Private Crypto in Cross-Border Payments

Private crypto promised fast, cheap global transfers. But in 2025, CBDCs processed $59 billion in cross-border transactions-up 45% from the year before. How? Because 29 countries are now part of formal cross-border CBDC initiatives like mBridge and Project Dunbar. These aren’t just tech demos. They’re live bilateral agreements between central banks to settle payments directly, without intermediaries. Compare that to Bitcoin or Ethereum. Even with Layer 2 solutions, users still need to convert fiat to crypto, wait for confirmations, pay gas fees, and then convert back. CBDCs skip all that. A payment from Singapore to Germany can settle in seconds, with no third-party exchange involved. And because these systems are built on shared standards, they’re interoperable by design.Regulation Isn’t a Bug-It’s the Feature

Crypto supporters love to say governments will never control money. But here’s the truth: most people don’t want to be in charge of their own financial compliance. They want to know their money won’t be frozen by a random validator, or seized because a blockchain analytics firm flagged a transaction. CBDCs solve that. 48% of countries running CBDC pilots have already aligned their AML and CFT rules with digital currency flows. 38% are testing blockchain-based identity systems to auto-verify users without manual paperwork. That’s not surveillance-it’s convenience. Imagine sending money to your family overseas and not having to answer 10 questions from your bank because the system already knows who you are. Private crypto, on the other hand, operates in legal gray zones. Exchanges get shut down. Wallets get blacklisted. Transactions get reversed. That’s not freedom-it’s instability.

The Bank Run Risk That No One Talks About

Here’s the scary part: if a CBDC is too attractive, people could pull all their money out of banks. The Atlantic Council warns that if citizens suddenly shift savings from commercial bank deposits to CBDCs, banks could lose the funds they use to lend for homes, businesses, and cars. Interest rates could spike. Credit could freeze. That’s why central banks aren’t launching CBDCs like a new app. They’re designing them with limits. India’s CBDC caps individual holdings. The ECB is testing non-interest-bearing CBDCs for small users. The goal isn’t to replace banks-it’s to coexist with them. CBDCs are meant to be a public payment layer, not a savings account replacement. Private crypto doesn’t face this problem because it doesn’t connect to the banking system. But that’s also its weakness. If you want to pay your rent, buy groceries, or get a loan, you still need fiat. Crypto can’t do that alone.Security: CBDCs Are Built for Resilience

Crypto wallets get hacked. Exchanges collapse. Rug pulls happen. In 2024 alone, over $3.2 billion was stolen from DeFi protocols and centralized exchanges. CBDCs are different. They’re built by central banks with decades of experience securing national financial infrastructure. Over 100 central banks are using CBDC development as a chance to upgrade outdated payment systems with modern encryption, zero-trust architectures, and real-time fraud detection. The IMF’s 2024 cyber resilience report confirms: CBDCs are being designed with fail-safes that crypto networks simply don’t have. Yes, CBDCs create new attack surfaces. But they’re also backed by national security agencies, military-grade infrastructure, and continuous monitoring. Private crypto? It’s a Wild West with no sheriff.

Where Private Crypto Still Wins

Let’s be fair: CBDCs aren’t perfect. And private crypto still has advantages. If you live in a country with capital controls, CBDCs can’t help you bypass them. But Bitcoin can. If you want to send money without government oversight, crypto still wins. If you believe in decentralized governance-where no single entity controls the rules-then Ethereum or other DAO-driven networks are still your best bet. But here’s the catch: those use cases are niche. They matter to activists, hackers, and speculators. They don’t matter to the 80% of the world that just wants to pay bills, get paid, and send money home without fees or delays.The Real Battlefield: Financial Inclusion

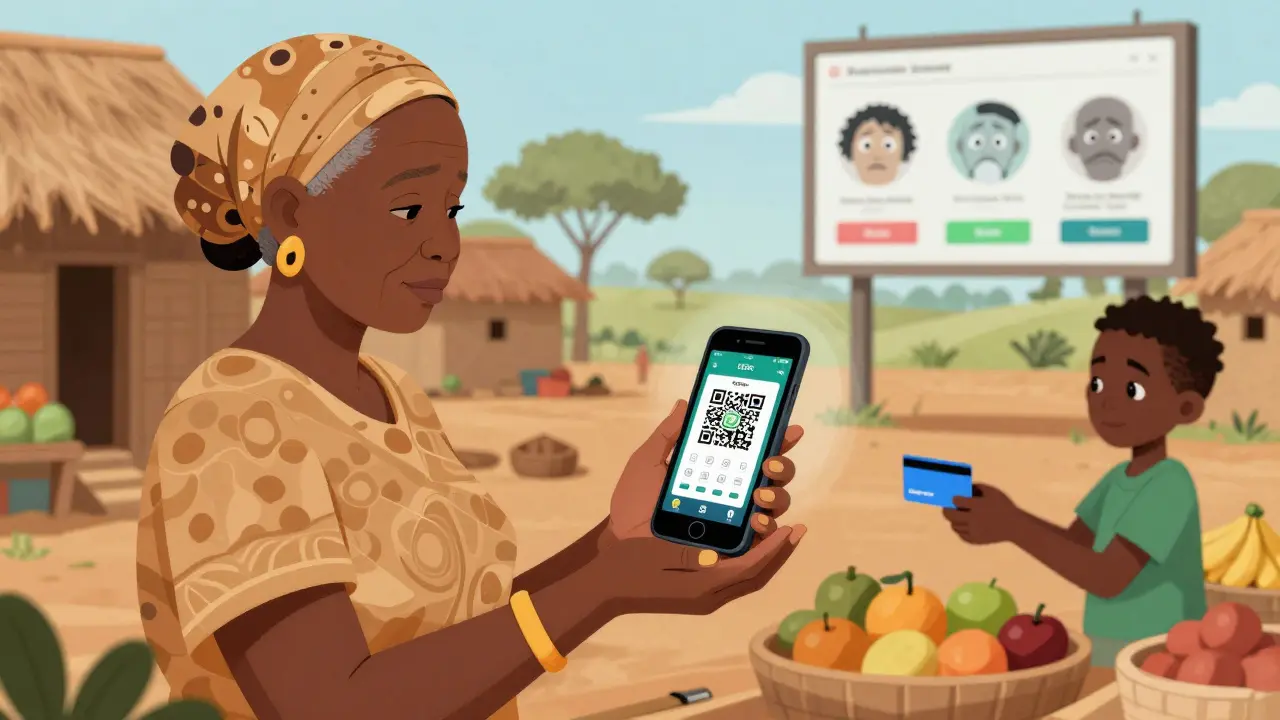

The UN Development Programme reports that over 1.4 billion adults still don’t have bank accounts. Many live in rural areas with no ATMs, no internet, and no smartphones. Private crypto can’t reach them. You need a wallet, a seed phrase, a smartphone, and literacy in digital finance. CBDCs are being designed for exactly these people. India’s CBDC works offline via NFC. Nigeria’s eNaira can be accessed via basic USSD codes on old phones. Jamaica’s platform lets users pay with QR codes-even without a bank account. This isn’t tech for the elite. It’s infrastructure for the excluded. Private crypto hasn’t cracked this. It’s still stuck in urban tech hubs. CBDCs are already being deployed in villages.What Comes Next?

By 2027, expect at least 20 more countries to launch CBDCs. The G20 nations are coordinating standards. The IMF is pushing for global interoperability. China’s digital yuan is already being used in over 100 countries for trade settlements. Private crypto won’t disappear. But its role is shrinking. It’s no longer the future of money-it’s becoming a niche asset class, like gold or collectibles. CBDCs are becoming the plumbing of the global economy. The winners? People who can pay instantly across borders. Small businesses that don’t pay 3% in processing fees. Farmers in Kenya who get paid the same day. Grandparents who send money to grandkids without a smartphone. The losers? The myth that money must be decentralized to be free. Sometimes, the most powerful thing you can do is let someone else handle the complexity-so you don’t have to.

Alex Strachan

So CBDCs are the new iPhone? Just sleek, silent, and totally locked down. 🤖💸

Emily L

Wow so now the government gets to decide who gets to spend their own money? Cool. Just cool.

surendra meena

THIS IS THE END OF FREEDOM!!! THEY’RE WATCHING EVERY CENT YOU SPEND!!! NO MORE ANONYMOUS TRANSACTIONS!!!

Adam Hull

Let’s be honest: CBDCs are just fiat with better UI and zero innovation. The real revolution died when Satoshi vanished.

Phil McGinnis

It’s amusing how people mistake efficiency for freedom. CBDCs are not a threat-they’re an inevitability. The state has always controlled money. This is merely modernization.

Kevin Gilchrist

They say ‘convenience’ but what they mean is control. I don’t want my grandma’s pension frozen because some algorithm decided her grocery purchase looked ‘suspicious.’ This isn’t progress-it’s dystopia dressed in UX.

Bianca Martins

India’s offline CBDC via NFC? That’s actually brilliant. I’ve seen villages there with no banks but tons of old phones. This could change lives. Not perfect, but way better than nothing.

prashant choudhari

CBDCs in India are working. No drama. No hype. Just payments. People are using it for daily groceries, school fees, and rickshaw fares. It’s quiet. It’s real.

Prateek Chitransh

Interesting how you call crypto’s volatility ‘instability’ but ignore that CBDCs can be turned off by a single government. That’s not security-that’s fragility.

Andy Reynolds

Let’s not forget who this is really for: the unbanked. Not the crypto bros. Not the Wall Street bots. The mom in Lagos sending cash to her sister in Accra with a basic phone. That’s the real win here.

Mandy McDonald Hodge

i just wish theyd make the app less glitchy tho like i tried to pay for my coffee and it said ‘transaction failed please try again’ and i was already late for work 😭

Josh Seeto

CBDCs process $59B in cross-border payments? Funny-Bitcoin’s Lightning Network does $1.2B monthly. You’re comparing a highway to a bicycle lane and calling it a victory.

Brandon Woodard

Let me get this straight: you’re defending surveillance infrastructure because it’s ‘convenient’? That’s not innovation. That’s surrender.

christopher charles

My cousin in rural Bihar uses eNaira to get paid for his pottery. No bank. No app. Just a phone call and a code. That’s magic. Not perfect, but better than what we had.

Bruce Morrison

CBDCs aren’t about control. They’re about resilience. After the 2023 banking crisis, countries realized they needed a public payment backbone. This isn’t oppression-it’s insurance.

Shawn Roberts

so crypto is dead? lol okay then why is everyone still buying btc like its going outta style 🤡

Daniel Verreault

Y’all keep acting like CBDCs are this sinister takeover… bro, if you think your bank isn’t already tracking your spending, you’ve never read the TOS. This is just… cleaner.

Khaitlynn Ashworth

Oh so now the government gets to decide if you can buy a toaster? Great. Next they’ll tell you how many eggs you can eat. This is fascism with a QR code.

Johnny Delirious

The argument that CBDCs serve the unbanked is disingenuous. Financial inclusion requires infrastructure, education, and trust-not a digital ledger controlled by a central authority.

Elisabeth Rigo Andrews

CBDCs are the new surveillance capitalism. They’re not replacing banks-they’re replacing autonomy. And you’re celebrating it because you’re too tired to care.

Vernon Hughes

In Nigeria, eNaira is used by street vendors who’ve never seen a bank. In Jamaica, it’s grandparents paying for medicine. This isn’t about control. It’s about dignity.

Rick Hengehold

Stop romanticizing crypto. It’s a casino with blockchain glitter. CBDCs are the plumbing. Nobody sees it. But everything works because of it.

Ian Koerich Maciel

While I appreciate the technical elegance of CBDCs, I remain deeply concerned about the erosion of financial privacy. The convenience of instant settlement does not outweigh the risk of permanent transactional surveillance.

Adam Hull

And yet, here we are. The same people who screamed ‘decentralize everything!’ now cheer for a state-run digital dollar. The irony is thicker than a 2024 Bitcoin whale’s portfolio.