Legal Framework for RWA Tokens: A 2026 Guide to Compliance & Structure

Imagine buying a slice of a Manhattan skyscraper or a vintage Rolex without dealing with banks, lawyers, or endless paperwork. That is the promise of RWA tokens, which are digital representations of ownership rights in physical or intangible real-world assets like real estate, commodities, and art, recorded on a blockchain. But here is the catch: you cannot just mint a token and claim it owns a building. The law does not care about your code; it cares about title deeds, securities regulations, and tax liabilities.

In 2026, the gap between blockchain technology and traditional finance has narrowed, but it hasn't closed. The legal framework for RWA tokenization is no longer a gray area-it is a complex maze of international regulations, specifically designed structures, and strict compliance requirements. If you get the legal structure wrong, your tokens are worthless digital collectibles, not enforceable financial instruments. Let’s break down how this framework actually works, where it stands today, and what you need to do to stay compliant.

The Core Legal Question: Token vs. Contract

Before writing a single line of smart contract code, you must answer one fundamental question: Does the token itself represent legal ownership, or is it merely a contractual claim against a custodian? This distinction defines your entire legal strategy.

In most jurisdictions today, courts do not recognize a blockchain ledger as a valid land registry or securities depository. You cannot point to a transaction hash and prove you own a house. Instead, the industry relies on two primary models:

- Direct Asset Tokenization: The token represents direct ownership of the asset. This is rare because few legal systems allow a blockchain entry to replace a government-issued title deed. It faces massive regulatory hurdles regarding non-fungibility and transferability.

- Tokenized Special Purpose Vehicle (SPV): Also known as indirect tokenization, this is the industry standard. An entity-usually a private limited company or a trust-holds the actual asset. The tokens represent shares or beneficial interests in that SPV. When you buy the token, you are buying a piece of the company that owns the asset, not the asset itself.

This SPV model is crucial because it fits neatly into existing corporate and securities laws. It isolates liability-if one property fails, it doesn’t drag down other assets held in separate SPVs. However, it means your investors rely on the legal strength of the SPV’s contracts, not just the immutability of the blockchain.

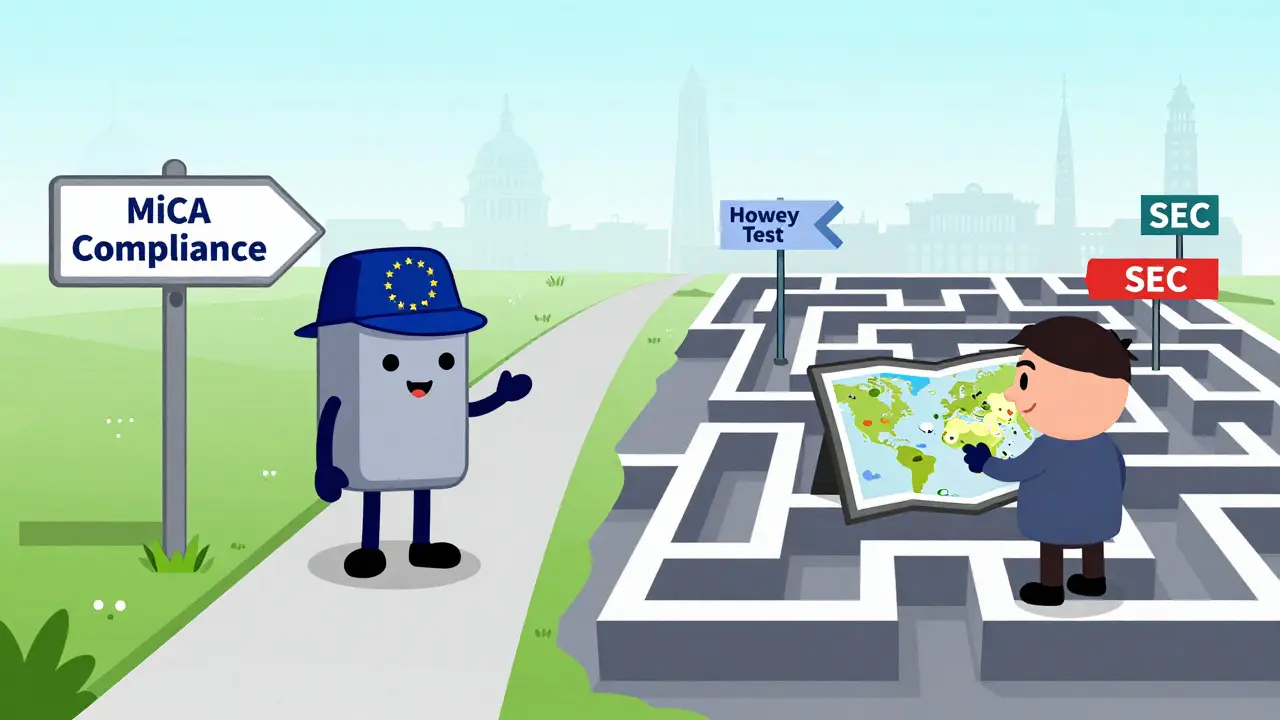

Global Regulatory Landscapes: EU vs. US

There is no global law for RWA tokens. Where you incorporate your SPV and where your investors live determines which rules apply. As of 2026, the European Union and the United States offer two very different paths.

| Jurisdiction | Key Regulation | Approach to RWAs | Compliance Burden |

|---|---|---|---|

| European Union | MiCA (Markets in Crypto-Assets) | Clear classification for utility and asset-referenced tokens; strong legal certainty for non-security tokens. | Moderate; requires AML/KYC and Travel Rule compliance. |

| United States | Securities Act of 1933 / Howey Test | Most RWA tokens are classified as securities, requiring registration or exemption (Reg D, Reg A+). | High; fragmented state/federal oversight, aggressive SEC enforcement. |

| Singapore | Payment Services Act (PSA) | Supportive sandbox environment; clear guidelines for digital payment tokens and security tokens. | Moderate; focused on anti-money laundering and investor protection. |

The European Union's MiCA regulation, fully effective since June 2023, provides a comprehensive handbook for issuers. It clarifies that many RWA tokens fall under "asset-referenced tokens" or "electronic money tokens," offering a clear path to market access across all EU member states. In contrast, the U.S. still relies on the Howey Test, a decades-old legal standard that often classifies RWA tokens as unregistered securities. This forces U.S. projects to navigate complex exemptions like Regulation D (for accredited investors only) or Regulation A+ (a mini-IPO process), which are expensive and time-consuming.

Structuring Your RWA Project: Step-by-Step

Building a compliant RWA project is less about coding and more about legal architecture. Here is the practical workflow used by successful firms in 2026:

- Asset Selection & Valuation: Choose assets with clear, verifiable titles. Real estate, treasury bills, and fine art are common. Ensure the asset can be legally transferred to an SPV. Independent valuation is mandatory to prevent fraud claims.

- Entity Formation: Establish an SPV in a jurisdiction friendly to tokenization. Popular choices include Switzerland, Singapore, Dubai (VARA), and Delaware (for U.S.-focused projects). Use Series LLCs if holding multiple assets to ring-fence liabilities.

- Legal Opinion: Hire specialized counsel to issue a formal memorandum. This document confirms whether your tokens are securities, what exemptions apply, and how they comply with local laws. This costs $50,000-$250,000 but prevents shutdowns later.

- Smart Contract Development: Code the token to enforce legal restrictions. For example, if your token is only for accredited investors, the smart contract must integrate with a KYC provider to block transfers to unverified wallets.

- Custody & Insurance: Partner with a licensed custodian to hold the underlying asset and the private keys. Never let the issuer hold both. This separation is critical for investor trust and regulatory approval.

Compliance Essentials: AML, KYC, and the Travel Rule

You cannot sell RWA tokens anonymously. Because these tokens represent real economic value and often yield returns, regulators treat them like traditional financial products. This means strict adherence to Anti-Money Laundering (AML) and Know Your Customer (KYC) protocols.

The Travel Rule (Regulation (EU) 2023/1113 in Europe and similar FATF standards globally) requires that every crypto-asset transfer includes specific information about the sender and receiver. For RWA platforms, this means integrating identity verification directly into the user journey. Before a user can buy a token, their identity must be verified. Before they can sell, the buyer must be vetted. Failure to implement this leads to heavy fines and potential criminal charges for the platform operators.

Additionally, the Digital Operational Resilience Act (DORA), effective January 2025 in the EU, imposes strict cybersecurity requirements on financial entities. RWA platforms must demonstrate robust IT infrastructure, incident reporting mechanisms, and third-party risk management. This is not optional; it is a license-to-operate requirement.

Pitfalls to Avoid: Lessons from Failed Projects

History is littered with RWA projects that failed due to legal oversights. Consider the case of a 2024 art tokenization platform that collapsed. They used a "direct tokenization" model, claiming tokens represented direct ownership of paintings. When the platform went insolvent, token holders were treated as unsecured creditors, not asset owners, because there was no legal wrapper linking the token to the physical art. They lost everything.

Conversely, successful projects like InvestaX used a Singaporean SPV to hold property titles. Tokens represented beneficial ownership interests in the SPV. When disputes arose, investors had clear contractual remedies under Singaporean law. The lesson is clear: the legal wrapper is more important than the blockchain technology.

Common mistakes include:

- Misclassification: Treating a security token as a utility token to avoid registration.

- Ignoring Tax Implications: Failing to clarify capital gains tax responsibilities for token holders in different countries.

- Poor Title Integration: Not ensuring the SPV’s ownership of the asset is recognized by national registries.

- Lack of Liquidity Plans: Issuing tokens without a compliant secondary market mechanism, trapping investors.

The Future: Standardization and Institutional Adoption

By 2026, the RWA market is projected to reach nearly $24 billion. Institutional investors are entering the space, but only where legal clarity exists. The International Swaps and Derivatives Association (ISDA) is developing standardized legal documentation for RWA tokenization, which will reduce the cost and time of structuring deals. Expect to see more commercial real estate transactions in Europe using tokenization due to MiCA’s clarity.

For developers and entrepreneurs, the barrier to entry is no longer technical-it is legal. Success requires a multidisciplinary team: blockchain engineers, legal experts specializing in securities law, and traditional asset managers. The companies that thrive will be those that treat compliance as a core product feature, not an afterthought.

What is the difference between direct and indirect RWA tokenization?

Direct tokenization means the token itself represents legal ownership of the asset, which is rarely supported by current laws. Indirect tokenization uses a Special Purpose Vehicle (SPV) to hold the asset, with tokens representing shares or beneficial interests in that SPV. Indirect tokenization is the standard because it aligns with existing corporate and securities laws.

Is RWA tokenization legal in the United States?

Yes, but it is heavily regulated. Most RWA tokens are classified as securities under the Howey Test. Issuers must register with the SEC or use exemptions like Regulation D (for accredited investors) or Regulation A+. Non-compliant projects face severe enforcement actions.

How does MiCA affect RWA projects in Europe?

MiCA provides a unified legal framework for crypto-assets in the EU. It offers clear definitions for asset-referenced tokens and electronic money tokens, reducing regulatory uncertainty. However, it also mandates strict AML, KYC, and operational resilience requirements (via DORA) for all issuers.

Why is an SPV necessary for RWA tokenization?

An SPV isolates the asset from the issuer’s other business activities, protecting investors from cross-contamination of liabilities. It also allows the token to represent a legal interest in a recognized corporate entity, making it enforceable in court unlike a bare blockchain token.

What are the main risks of investing in RWA tokens?

Risks include regulatory changes, lack of liquidity if no compliant secondary market exists, smart contract bugs, and counterparty risk if the custodian or SPV manager fails. Investors should always verify the legal structure and ensure the underlying asset is properly titled and insured.